Following the release of the Annual Report and Financial Statements of International Hotel Investments p.l.c. (IHI) for 2024, the company hosted a presentation for financial intermediaries and the Malta Association of Small Shareholders on Thursday, May 8, 2025.

During the presentation, Simon Naudi, Group CEO and Managing Director of IHI, provided a concise but rigorous description of the company: International Hotel Investments p.l.c. (IHI) serves as a real estate investor, developer, and operator, with a particular emphasis on luxury hotels and serviced residences under the proprietary Corinthia Brand.

This straightforward definition highlights the diverse activities undertaken by IHI: real estate investment, development, and operation. This multifaceted approach that consolidates functions normally performed by separate organisations, enables Corinthia to integrate them into a cohesive set of operations. IHI’s main focus remains on luxury hotels and serviced residences that feature the Corinthia brand.

IHI’s goal is the continued growth of its Corinthia Brand as a significant player in the field of luxury accommodation, and in so doing, benefitting from the entire value chain of investment, development and management of luxury hotels and serviced residences.

Corinthia’s expansion is impressive. It is currently involved in 27 hotel operations and developments, using the Corinthia brand for luxury properties but also using other brands, including Verdi, for its other operations.

Corinthia brand is now recognised globally, and on this foundation, it is able to grow at a faster pace by way of :

1 strategic investments in hotel real estate developments ; and above all

2 providing brand, management and development expertise to other investors in return for management fees and carried interests in project returns.

When Corinthia began its operations in 1962, it chose the more challenging path of owning its own hotels, a decision that has proven beneficial due to the potential for property value appreciation. Corinthia has, however, extended its management services to third-party owned hotels, charging management fees while retaining its branding. This significantly enhances the overall operation.

Corinthia’s service companies have flowered further. The hotel management arm, Corinthia Hotels Limited CHL has expanded globally and continues to invest in human resources. C-REV – Corinthia’s real estate origination and development company is also expanding globally [formerly named CDI]. QP – Corinthia’s architectural design company has now established offices in London, Dubai and Asia and its services are currently widely provided to external companies, thus outgrowing its initial limited sphere of internal services provision.

Corinthia provides management services to: CorinthiaRome (to open 2025), Corinthia Doha (2026), Corinthia Yacht Club Doha, Corinthia Riyadh (2027), Corinthia Dubai (2029), Corinthia Bucharest,Corinthia Maldives (2027), The Surrey, a Corinthia New York, Vivaldi Malta, Verdi Gzira Malta, Panorama Prague.

Corinthia Bucharest

Simon Naudi added that negotiations are in progress on management and development agreements in the USA, the Gulf and Europe, with an initial eye being cast on the Far East

Apart from its service companies aforementioned, another main building block is offered through its owned hotels and strategic shareholdings, including Corinthia Palace Malta, Corinthia St George’s Malta, Corinthia Budapest, Corinthia St. Petersburg, Corinthia Lisbon, Corinthia Tripoli, its commercial centres in Tripoli and St. Petersburg, Verdi Hotel St George’s Bay, Grand Hotel Prague, Radisson St Julian’s Malta, Corinthia London (50% share), Corinthia Brussels (50% share),Corinthia Moscow (10%) Corinthia Beverly Hills (10%; under development) Corinthia Turks and Caicos (option for 50% share; under development) Corithia Oasis (Ħal-Ferħ, awaiting permits)

The Oasis

What are the highlights of 2024?

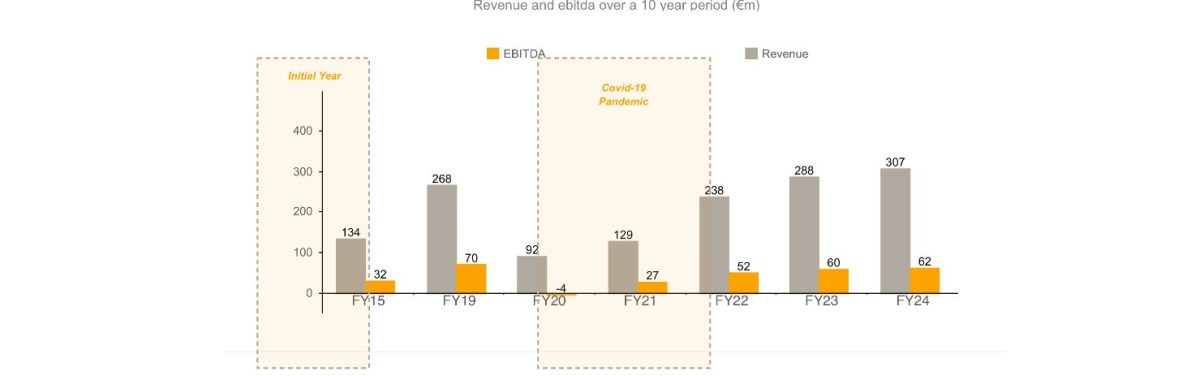

Simon Naudi noted that over the past 10 years, the Group has experienced significant growth. FY24 performance continued to improve over FY23 as the Group continued to recover from the pandemic. This chart bears this out graphically.

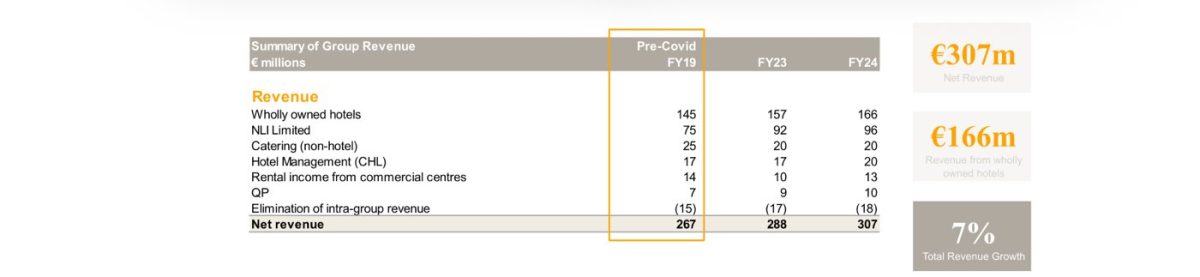

Total revenue is increasing by 7% from FY23, driven by significant growth in wholly owned hotels. See the following chart:

A focus on Hotel Gross Operating Profit (GOP):

The Group reports significant improvements in operating profits in hotel performance.

All hotels have exceeded pre-pandemic performance. Performance of Corinthia St Petersburg is still affected by continued geopolitical tensions. The hotel in Prague has been fully leased to a third party in FY24 and has thus been excluded.

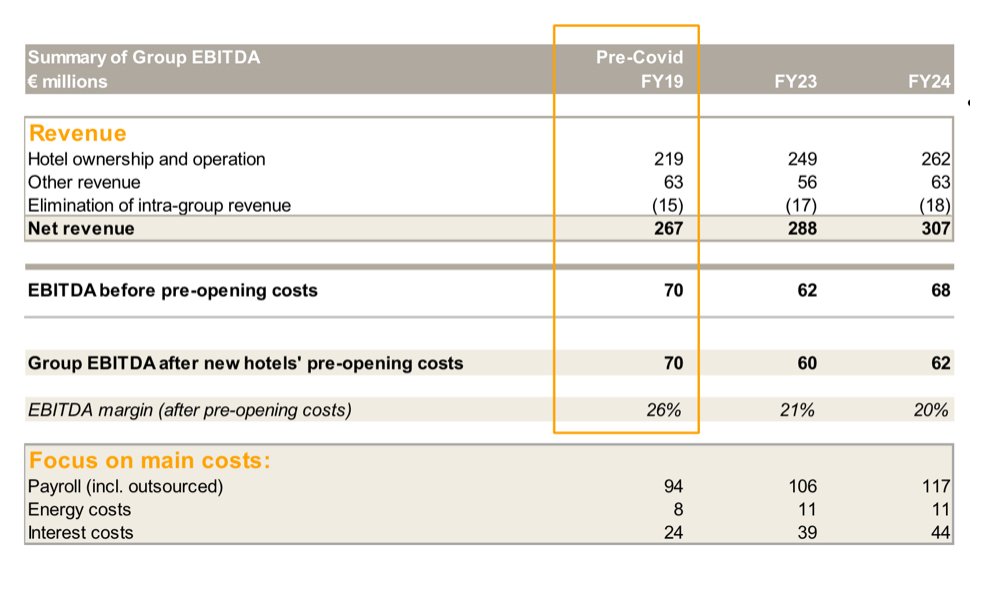

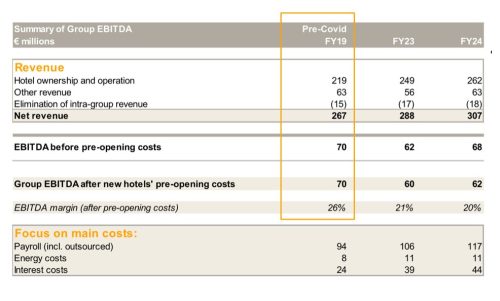

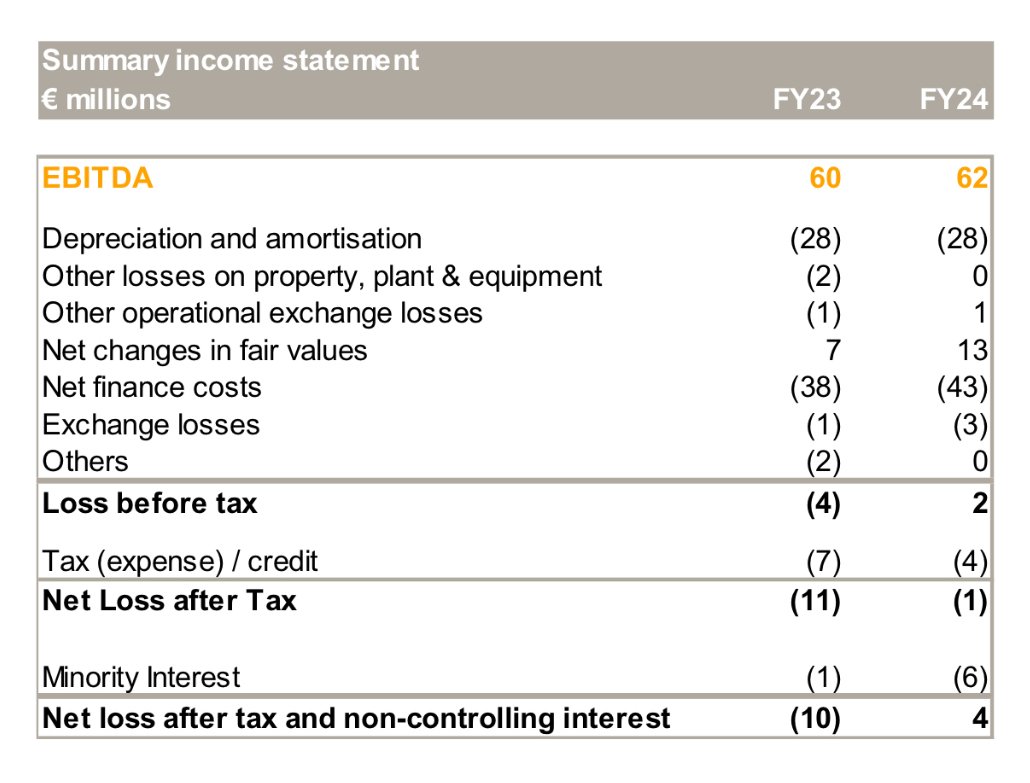

By an equal margin to revenue, the Group recorded an EBITDA of €62 million in FY24, notwithstanding cost pressures and operational investments in new operations.

The Group continues to exercise a tight handle on operating costs (such as payroll and energy costs) in an environment of adverse geopolitical developments, significant inflationary pressures and rising interest rates.

EBITDA in FY24 was mainly absorbed by depreciation, net finance costs and exchange differences.

Depreciation is in line with last year. The increase in finance costs is a reflection of the increased base rates in FY24 and the new loan drawdowns relating to new capex investments.

Changes in fair value for FY24 mainly relate to a net uplift in the assessed valuation of the Group’s investment property, namely: Tripoli Commercial Centre (+€3m), Corinthia Prague (+€2.6m), St Petersburg Commercial Centre (+€1m) and also to an impairment reversal on the Corinthia Hotel Tripoli (+€6.5m).

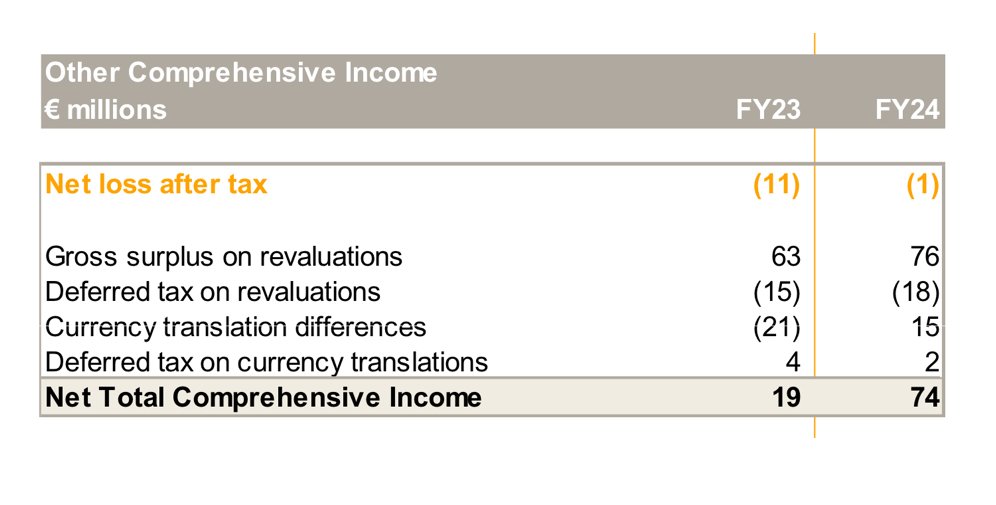

Net revaluation uplifts recognised in other comprehensive income (OCI) amounted to €75.9m on account of the improving performance of the Group’s owned hotels.

Main revaluation movements:

Corinthia Lisbon: €27.7m

uplift Corinthia London: €15.4m

uplift Golden Sands: €12m

uplift Corinthia Oasis: €9.3m

uplift Corinthia St. Petersburg: €8.3m

uplift Corinthia Prague: €6.3m

uplift Corinthia Budapest: €3m impairment

The gain on translation differences was mainly due to the strengthening of the Sterling.

The overall result for 2024 was of €74m in Total Comprehensive Income against €19m in 2023.

The Group’s total assets increased by c. €175 million in FY24, mainly driven by uplifts in value of our properties and continuing works on the Brussels project.

*An increase in total assets, from €1.77bn to €1.94bn was reported in FY24.

*Shareholders’ equity increased to €674.3 million from €613.3 million last year, translating into an NAV per share of €1.095 from €0.996 in FY23.

Additional notes:

*Independent valuation of CHL at €355 million approved by the auditors at €259 million & QP valued at €22.4 million. *As CHL and QP are internally generated businesses and are intangible in nature, uplifts arising from these values are recorded solely in the Holding Company in line with IFRS, but result in a combined Nav/share of €1.46.